http://www.intellecpoint.com/2016/11/is-ekovest-investible.html

After the article on Ekovest a month ago, its share price has since rose from circa RM1.95 to now around RM2.18.

(Before I deliberate on this topic, I would like to insist, I have always been very careful when putting my positive comments on a company as it has to be a long term value stock. My definition of a long term value stock is always about one potentially can be putting away his/her money for years as investments and the fundamental of the company has to be of creating value to its investors. Value investment is always a subject of debate as is it just an undervalued stock or is it also a very good company which will consistently provide better value than other companies among its peers. In my perspective, it is always more of the latter where it will continuously provide investment value, than the former i.e just cheap stocks but can also be poor in terms of business performance.)

Ekovest to me is putting itself to be a company with recurring revenue from its assets although at this moment, it is still more of a construction company. I will put the composition of its construction:property:toll businesses at the moment to be as follows 60:15:25. (I know, I am aware of how I described Gadang)

In 3-4 years down the road though, Ekovest is going to be a very different company. That is very important to me as its composition will be more like 35:15:50 in the order of construction:property:toll. Why?

Its toll business itself may potentially be even bigger than LITRAK. As it is, for DUKE 1, after its 6th to 7th year of operations it has started to register good profits (cashflow wise, would be even better). By the time DUKE 2 and SPE becomes operational, it could be a very substantial toll operator than a construction outfit. (I would be even more amazed if its construction arm is to be just as big, which means that it will be getting more jobs)

Yesterday, in a Q&A session, the CEO of EPF put down that for his private equity investments, he is looking at IRR of between 10% to 13%. He further mentioned,

“If you look at the types of assets that we have been investing in, they would typically have an IRR range of between 10% and 13%, depending on the risk profile of the assets, the tenure of the concessions and the security of cashflows

“For instance, a power plant asset which has secured power purchase agreements would be in the lower range, while something that has a bit more revenue volatility would be in the higher range,”

I will take it that for DUKE as it has some volatility, EPF is probably looking at around 11%. In today's low interest rate environment, where US is offering almost zero, 11% is very high. I would not mind putting my money in stable investment which returns 11% IRR.From that perspective, I will take the positives and negatives - if I am an investor of Ekovest, it is willing to let go 40% for 11% IRR, this is a negative. I am sure that it can get better deals elsewhere.

From a positive standpoint, Ekovest still has 60% of that asset which it stands to gain 11% IRR at valuetion of (RM2.825 billion) still for more than 40 years (in fact more, as a concession investment such as DUKE has a definite concession period, hence when doing a DCF it will take into account that definite period - not indefinite period in which case they use terminal value). So for any investors, even putting money for DUKE already has his money worth with very strong IRR. For me, if the IRR of 11% is right, Ekovest's 60% ownership could translate into at least a good multiple of what the EPF is paying for as concession assets has good value - just look at LITRAK which still enjoys 16x PE despite its concession to remain around 15 years?

And as mentioned in previous article, what about Ekovest's other assets such as SPE, its construction business and property projects? They must have worth some good numbers as well.

Is it investible though?

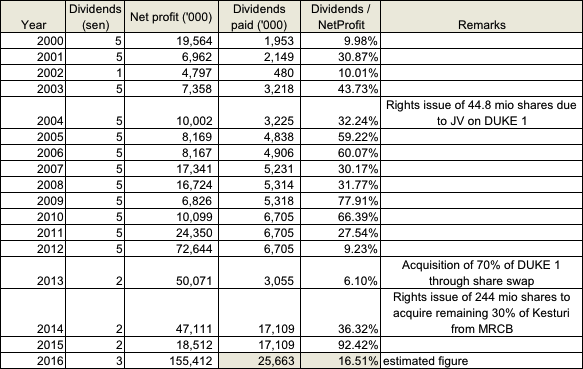

Now, after the above, is Ekovest an investible stock? There are several benchmarks to a company. Firstly, even if it is to make money, bring in good cashflow (remember, some red chips (China's) companies showed profits, cashflow but without or little dividends) - would the management be ready to share part of it in the form of dividends? Here are the track record of the company's dividend payment since 2000.

|

| Dividend and net profit of Ekovest from FY2000 to 2016 |

The management has mentioned of its willingness to pay some of its return of RM1.13 billion to shareholders. That has yet to be announced. If I am to read its cashflow requirement, the amount should not be too low - i.e. less than RM100 million.

Another thing which was of concern to me was that the free float for Ekovest was way too low for some time - somewhere in the range of 5% to 10% as it is still a very tightly held stock - through Lim Kang Hoo's family, Haris Hussein (brother of Hishamuddin Hussein) and an old partner of Lim Kang Hoo, Khoo Nang Seng. In the last few months, the two groups except for Lim Kang Hoo has disposed off some of their shares. One may think that they are selling early which is a bad sign, but that has also translated into more liquidity for the market. (Frankly, I do not know how to read this.)

Ekovest has not been a much followed stock because funds do not like low liquidity stocks especially the sell side brokers. They are not able to introduce much to their clients as there are not much stocks to buy. That to me is changing for Ekovest. If I am to read right, some if not all portion of Haris Hussein's sale 6 months ago went to several funds.

As it is still at good value, I see the funds coming in a bigger way - as they are becoming visible for the bigger guys. That's how I see it as it is surfacing some of its value.